You know the moment. A customer walks into your store, picks up the phone, the laptop, the generator, and the furniture piece they clearly want. They check the price. They put it back down. They say they'll think about it. You both know they won't come back.

Or they message you on WhatsApp, you send the invoice, they read it, and then go quiet. Not because they don't want what you're selling. Because the full amount is a stretch right now.

This is the daily reality for thousands of Nigerian merchants. The frustrating part is that the customer was right there. They wanted the product. They needed it. The gap was cash flow, not desire.

Nigerian consumers are price-sensitive and instalment-minded. This is rational behaviour in an economy where income often arrives monthly, but spending needs don't. The informal "pay small small" arrangements that merchants have always navigated (writing in notebooks, chasing payments, absorbing bad debt) are proof that demand for spread payments has always existed. What hasn't existed, until recently, is a structured, merchant-safe way to offer it.

That's what Buy Now, Pay Later (BNPL) solves. If you're a Nigerian merchant who hasn't yet decided whether to offer it, this guide is written for you.

What Is BNPL? Key Terms Defined

Before examining the business case, it helps to understand exactly what BNPL is and what it isn't, particularly for a merchant audience that has heard conflicting descriptions.

Buy Now, Pay Later (BNPL): A short-term financing product that allows a customer to take immediate possession of a good or service and repay the cost in structured instalments over a fixed period. The financing is provided by a third-party provider, not the merchant. The merchant receives payment promptly; the provider manages the credit relationship with the customer.

Average Order Value (AOV): The average monetary value of a single transaction. When merchants offer BNPL, customers are no longer constrained by what they can afford upfront, which typically increases the value of each basket. A customer who would have bought a ₦90,000 device often upgrades to the ₦150,000 model when the full cost doesn't have to land at once.

Conversion Rate: The percentage of customer interactions that result in a completed sale. A customer who enquires, browses, or adds to cart but doesn't pay is an unconverted lead. BNPL addresses the payment friction that causes abandoned transactions.

Customer Acquisition Cost (CAC): The total cost of acquiring a new paying customer, including marketing, promotions, and sales effort. When BNPL makes a merchant more discoverable and more appealing to price-sensitive buyers, more customers arrive organically, and fewer require heavy promotional spend to convert.

Merchant Settlement: In a BNPL transaction, settlement refers to when and how the merchant receives their payment. Under a well-structured BNPL model, settlement happens promptly after the transaction is confirmed, regardless of the customer's repayment schedule. The merchant bears no collection risk.

The Nigerian BNPL Market: What the Numbers Show

Understanding the scale of the opportunity requires looking at verified market data, not anecdote.

Nigeria's BNPL market was valued at approximately USD 1.55 billion in 2025 and is projected to grow to USD 3.96 billion by 2031, representing a compound annual growth rate of 16.1%. The market grew at a CAGR of 25.9% between 2022 and 2025, making Nigeria one of the fastest-expanding BNPL markets on the continent.

Nigeria's BNPL sector is expanding rapidly, driven by increasing consumer demand for flexible payment solutions. Several factors contribute to this expansion, with e-commerce growth playing a central role by creating demand for instalment-based payment options.

The driver isn't a novelty. In Nigeria, mobile money services and super apps are driving adoption, while e-commerce platforms are increasingly incorporating BNPL options to attract more customers. Jumia, Nigeria's largest e-commerce platform, partnered with instalment providers in 2024 specifically to extend BNPL at checkout.

For a merchant, this data answers one foundational question: Is there genuine consumer demand for BNPL in Nigeria? The answer is clearly yes, and it is growing every year.

What BNPL Actually Means for the Merchant

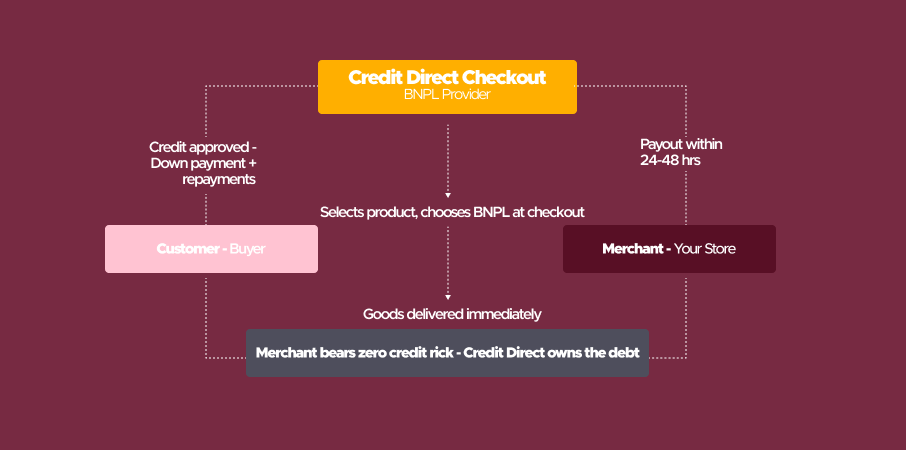

How does the money flow?

A customer selects your product and chooses BNPL at checkout. They pay a down payment upfront (typically a percentage of the purchase price), and the BNPL provider extends credit for the remainder, which the customer repays in scheduled instalments. The merchant gets paid promptly. The credit relationship sits between the customer and the BNPL provider.

Who bears the default risk?

The BNPL provider does. This is the critical structural difference between BNPL and the informal credit many Nigerian merchants already extend. When you let a customer take goods on a promise to pay you later, you are the lender: you bear the risk of non-payment, carry the debt on your books, and make the follow-up calls. With a BNPL provider, none of that is your problem. The provider has done the credit assessment, approved the customer's limit, and owns the collection process. Your job ends at the point of sale.

When do you get paid?

With Credit Direct Checkout, merchant payouts land in your business wallet typically within 24 to 48 hours of the transaction. You are not waiting for the customer to complete their instalment plan. The credit risk sits with Credit Direct.

The Economics: How BNPL Moves the Numbers That Matter

Average Order Value Goes Up

Klarna's merchant base reports a 45% increase in average order value when shoppers pay over four payments. Affirm reports an 85% increase in average order value when consumers use its BNPL plan over other payment methods.

These are global figures. The specific uplift varies by category and market, but the mechanism is consistent: when customers are no longer constrained by what they can pay upfront, they choose better. The merchant who previously watched customers buy the ₦90,000 phone instead of the ₦150,000 model now has a credible way to close the upgrade. BNPL merchants using Credit Direct Checkout have seen average order values increase meaningfully.

For merchants in high-ticket categories (electronics, furniture, home appliances, solar energy systems, fitness equipment), this represents a direct, measurable increase in revenue per transaction.

Conversion Rates Improve

RBC Capital Markets estimates that a BNPL option increases retail conversion rates by 20% to 30% and lifts the average ticket size by 30% to 50%.

A Stripe experiment across more than 150,000 global payment sessions found that businesses saw up to a 14% increase in revenue when a BNPL payment option was available, driven by higher conversion rates and higher average order values. More than two-thirds of BNPL volume came from net-new sales, suggesting that customers only completed these transactions because BNPL was offered.

To put this in practical terms: if your store currently converts 20 out of every 100 serious enquiries into sales, a 50% improvement in conversion takes that to 30. On the same traffic, the same footfall, the same WhatsApp enquiries, and the same store overhead, you close 50% more transactions.

Cart Abandonment Falls

29% of buyers abandon their shopping carts due to a lack of flexible payment methods. 55% of BNPL users choose the option because it allows them to afford things they otherwise couldn't.

These aren't low-intent browsers. They are motivated buyers being turned away by a payment structure that doesn't fit their cash flow. BNPL addresses that at the point of intent.

Customer Acquisition Cost Drops

When word spreads that you offer flexible payment (and in Nigeria, word spreads fast), customers come looking for you specifically. Your product, combined with payment flexibility, is a differentiated offer. Credit Direct Checkout merchants report a customer acquisition cost reduction of up to 25%, driven by organic inbound demand from customers who are already looking for a BNPL-accepting merchant in your category.

Repeat Business Increases

Customers who use BNPL and have a good experience are significantly more likely to return. They've already completed onboarding; their credit limit is established; the next purchase is frictionless. For merchants, this makes BNPL a retention mechanism as much as a conversion tool.

How Credit Direct Checkout Works: The Merchant Experience

Credit Direct Checkout is a BNPL solution built specifically for the Nigerian market, operated by Credit Direct Finance Company Limited, an authorised and regulated financial institution by the Central Bank of Nigeria. This regulatory standing is significant: CBN oversight ensures consumer protections, responsible lending standards, and a compliance framework that keeps the platform operating sustainably.

Here is what the merchant journey looks like.

Step 1: Get Listed on the Platform

You apply to become a Credit Direct Checkout merchant via: https://www.creditdirect.ng/credit-direct-checkout#cdc-cta. The platform currently lists over 500 active retail stores across categories, including Gadgets & Accessories, Home & Kitchen Appliances, Furniture, Lifestyle, Solar Energy, Security, Fitness Equipment, and Supermarket.

Once onboarded, your store appears on the Credit Direct Checkout merchant directory, which is actively browsed by Credit Direct's existing customer base. Your business becomes discoverable by pre-qualified shoppers who already have an approved credit limit in their accounts and are ready to spend.

Step 2: Choose Your Merchant Channels

Credit Direct Checkout supports in-store, website, and WhatsApp transactions. This matters because a large portion of Nigerian commerce happens through messaging channels. A merchant can close a BNPL transaction via WhatsApp without a purpose-built e-commerce setup, which removes a major adoption barrier for smaller merchants.

Step 3: How the Customer Qualifies for BNPL

For your customer, the requirements are straightforward:

- Active bank account (for eligibility assessment)

- Active email address (to receive transaction updates)

- BVN and BVN-registered phone number (for identity verification)

- Active ATM card (for the down payment and future instalments)

Customers can check how much credit they qualify for in under five minutes through the Credit Direct app or website, with limits of up to ₦1 million available. Most Nigerians with a smartphone and a bank account meet the eligibility criteria. The product is built for the mainstream Nigerian working adult.

Step 4: Payout to Your Business Wallet

Payment lands in your Credit Direct Business wallet promptly after the transaction. From there, you can make business transactions or leave the funds working for you.

The Revenue Loop Most Merchants Miss

Here is something that goes beyond the BNPL transaction itself.

When your BNPL payouts land in your Credit Direct Business wallet, those funds can earn returns of up to 15% per annum on a daily basis. This is a feature of the Credit Direct Business wallet that allows your business to earn on funds between their arrival and your deployment.

Consider the sequence. You make a sale. The customer pays over time. You receive your payout promptly. That payout sits in your wallet, earning a daily return until you use it for inventory, operational costs, or your next business cycle.

The logic is the same as keeping working capital in a high-yield account rather than a static current account: lower friction, a more competitive rate, and no lock-in. Routing revenue through the wallet intentionally and timing transfers with operational needs means extracting value at every stage of the money cycle, not just at the point of sale.

You can explore the full scope of the Credit Direct Business offer at www.creditdirect.ng/business.

A Real Merchant in the Ecosystem: vivo Nigeria

In April 2026, Credit Direct and vivo Nigeria signed a formal partnership, making vivo one of Credit Direct Checkout's anchor merchant partners. The agreement targets sales of over 200,000 devices, with Credit Direct providing the BNPL financing that makes those devices accessible to customers who would otherwise be priced out of the mid-range and flagship tiers.

For Credit Direct, it is the company's first formal partnership with vivo Nigeria and a direct expression of its core purpose: extending financial access to individuals excluded from traditional credit. For vivo, it opens its products to a substantially wider pool of buyers without changing its pricing structure or incurring any credit exposure.

Smartphones sit squarely in the category where BNPL produces the clearest results: high desire, high price sensitivity, a strong upgrade cycle, and a meaningful price gap between entry-level and aspirational models. When a customer can spread the cost of a mid-range device, the decision to upgrade becomes significantly easier.

For independent phone retailers, the implication is direct. The brands you stock are now attached to a BNPL offer at the brand level. Having the same capability in your own store is how you compete on equal terms, rather than sending a customer to a brand outlet that can close the sale you opened.

Is BNPL Right for Your Business? A Decision Framework

Some categories and business models benefit from BNPL more than others. Here is a practical framework.

BNPL is most valuable for you if:

Your average transaction value is above ₦30,000. Below this threshold, the BNPL process may introduce more friction than the conversion benefit justifies. Above it, payment flexibility becomes a genuine purchase decision factor.

You regularly hear customers say they'll "come back" or "think about it." This is the clearest signal that price friction is costing you sales. BNPL addresses this at the point of intent.

You sell in a category where customers frequently compromise. Electronics, furniture, appliances, fashion, fitness equipment, solar energy systems: these are categories with strong upgrade potential that BNPL is designed to unlock.

Your customers are salaried or have predictable income. Credit Direct Checkout is well-suited for the Nigerian salaried worker and working-adult demographic. If this describes your customer base, the credit assessment process is built with them in mind.

You operate on WhatsApp, in-store, or online. BNPL's value is only realised when customers can actually use it in your selling environment.

The practical requirements to get started are low. You need a registered business, a bank account, and the ability to process transactions in-store, online, or via WhatsApp. A complex e-commerce infrastructure is not a prerequisite.

How to Get Started

The process of becoming a Credit Direct Checkout merchant begins at www.creditdirect.ng/credit-direct-checkout. The onboarding process is designed to get you to your first transaction without unnecessary bureaucracy.

When you apply, you will specify your preferred channels (in-store, website, or WhatsApp) and the product categories you sell. Once approved, your store is listed on the platform and accessible to Credit Direct's customer base.

To explore the Credit Direct Business wallet and the yield it generates on your merchant payouts, visit www.creditdirect.ng/business.

What a Nigerian Merchant Actually Says

Eight Sage Limited is a Lagos-based distributor of household and office appliances: televisions, air conditioners, refrigerators, and generators. They sell across Nigeria through their website, offering last-mile delivery and pickup options. This is a business where average transaction values are high, customers are cost-conscious, and a single lost sale significantly impacts the bottom line.

Chief (Mrs) Moronke Fowode, Executive Director at Eight Sage, describes the impact of offering Credit Direct Checkout on their sales:

"Credit Direct has helped in increasing footfall to our website and, of course, the sales conversion has also been very good... Even if you have the full amount for a certain product, the fact that you have the ability to spread it means that you can use that money for other things on your wish list." — Chief (Mrs) Moronke Fowode, Executive Director, Eight Sage Ltd.

She emphasises that in an economy where the cost of goods has "skyrocketed," providing flexible payment options isn't just a luxury—it's a necessity for customers with steady incomes who want to manage their cash flow effectively.

Eight Sage operates in a category where BNPL produces the clearest results. A generator or refrigerator is often an essential purchase for Nigerian households and businesses. While the customer has a clear need, the upfront price is frequently the primary obstacle. BNPL removes that barrier, allowing the merchant to close the sale without compromising on their margins.

Frequently Asked Questions

What is BNPL for merchants in Nigeria? BNPL (Buy Now, Pay Later) for merchants is a payment model where a third-party provider extends credit to your customer so they can take a product immediately and pay in instalments. The merchant receives payment promptly from the provider. The provider manages the customer's credit and repayment. As a merchant, you get the sale without extending credit yourself or carrying any collection risk.

When do merchants get paid with BNPL? With Credit Direct Checkout, merchants receive payouts to their business wallet within 24 to 48 hours of the transaction. You do not wait for the customer to complete their instalment plan.

Does offering BNPL increase sales? Yes. Customers who show interest but are unable to afford the lump-sum price for a product are typically not likely to buy. With BNPL, your chances of closing a sale are much higher.

Who bears the risk if a customer defaults? The BNPL provider does. In a properly structured BNPL arrangement, the credit risk sits entirely with the provider, not with the merchant. This is the key structural difference between BNPL and informal credit extended directly by the merchant.

What kinds of businesses benefit most from BNPL? Merchants with average transaction values above ₦30,000 typically see the clearest benefit. High-ticket categories, including electronics, furniture, home appliances, solar energy, fitness equipment, and fashion, are the strongest fits. Any business where customers regularly ask to pay in instalments or frequently compromise to a lower-value item is a good candidate.

Is BNPL regulated in Nigeria? Yes. Credit Direct Finance Company Limited is authorised and regulated by the Central Bank of Nigeria. The CBN has also introduced broader guidelines for digital lenders, including BNPL providers, covering responsible lending standards and consumer protections.

What does a merchant need to offer Credit Direct Checkout? A registered business, a bank account, and the ability to process transactions in-store, on a website, or via WhatsApp. A complex e-commerce setup is not required.

Can merchants earn on their BNPL payouts? Yes. Payouts from Credit Direct Checkout land in a Credit Direct Business wallet that earns up to 15% per annum on a daily basis. Merchants who route revenue through the wallet before deployment earn a return on funds that would otherwise sit idle in a current account.

The Bottom Line

Nigeria's BNPL market was worth USD 1.55 billion in 2025 and is on track to reach USD 3.96 billion by 2031. That growth is driven by real consumer demand: customers who want to buy, have the income to repay, and simply need a payment structure that fits their cash flow.

Every merchant reading this article has lost a sale this week to price friction: a customer who wanted the product, needed it, and walked away because the full amount didn't work right now. BNPL converts those moments by introducing a structured, provider-backed payment option that enables the purchase without changing your pricing or risk profile.

Early adopters in any category build a real differentiation advantage. The customers are already looking for merchants who accept BNPL. The question is whether they find your store when they do.

Credit Direct Finance Company Limited is authorised and regulated by the Central Bank of Nigeria. To list your business on Credit Direct Checkout, visit www.creditdirect.ng/credit-direct-checkout. For business wallet and revenue management features, visit www.creditdirect.ng/business.

%20compressed.png)