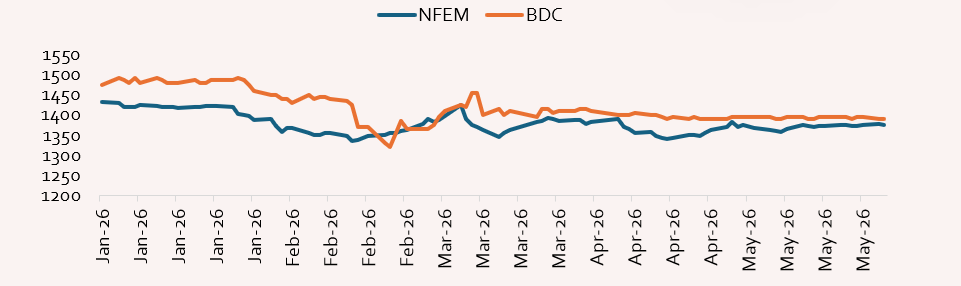

The Naira depreciated in May relative to April at the official window (NFEM), settling at an average of ₦1,370.05/$ compared to ₦1,362.42/$ in April. The lingering geopolitical tension between the United States and Iran kept crude oil prices above $100 per barrel in May, translating to higher domestic inflation via elevated PMS costs and imported inflation, both of which weighed on the Naira by stoking broader cost pressure sand FX demand from import-dependent sectors.

At the parallel market, the Naira strengthened by 14bps in May, with the BDC average rate settling at ₦1,392.76/$. This appreciation tightened the spread between the official and parallel windows to 2.01%, down from 3.67% in April, reducing arbitrage incentives and signaling improved pricing alignment across both markets.

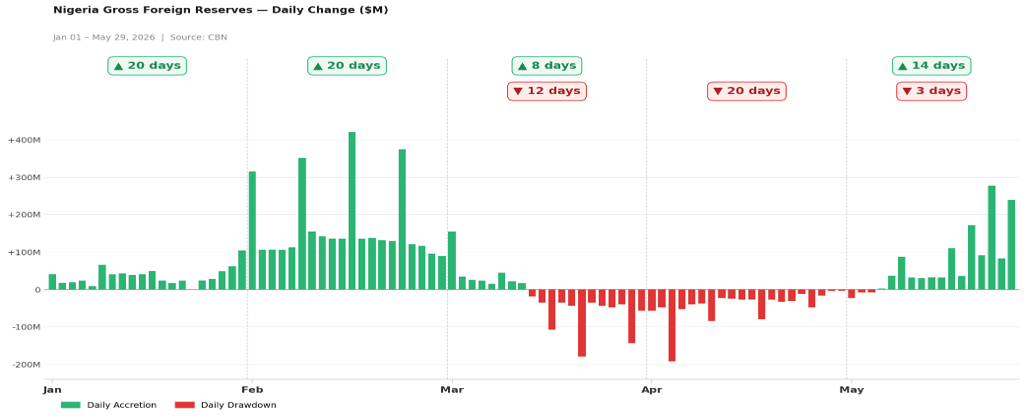

Nigeria’s gross foreign reserves rebounded by approximately $1.22bn, reversing two consecutive monthly decline, likely reaping the gains from elevated oil prices (Bonny light averaged $112.05/b in May) and reduced FPI pressures, with net equity outflows dropping to $6.61bn in April from $7.47bn in March. Further supporting the external position, S&P Global upgraded Nigeria’s sovereign credit rating to ‘B’ from ‘B-’ on May 15, 2026, citing FX reforms, stronger reserves, and improved fiscal fundamentals, a development that could modestly attract fresh portfolio inflows and lower Nigeria’s external borrowing costs over the medium term.

Expectation for June 2026: Fundamental vs Sentiments

FX Supply

- Crude Oil: Bonny light price peaked at $137.01/bl on April 07 and remained above $100, supporting positive FX earnings expectation and providing a buffer for Naira offsetting weaker crude oil output.

- Capital Importation: The recently released Q1 2026 data showed total capital importation surging 83.83% to $10.37bn, led by FPI at $9.86bn, signaling strong investor confidence and a positive sentiment outlook for the Naira.

- Trade Balance: The recently released Q1 2026 data showed the trade surplus hitting a record high of ₦7.55trn, signaling a structurally stronger external position and bolstering confidence in FX liquidity for June.

- Remittances: Diaspora remittances climbed to $107.4m. While lagged, diaspora inflows have been consistently stable and provide a structural non-oil FX buffer, partially cushioning against oil price volatility.

- External Borrowing: The recently approved $6bn multilateral borrowing is expected to supplement near-term FX supply and support reserve accretion. However, with external debt already at ₦74.4trn, the approval also signals rising medium-term debt service obligations.

FX Demand

- Import Dependency: The recently released Q1 2026 data showed imports declining 18.17% Y-o-Y toN13.62trn, easing USD demand pressure. However, lingering dependence on imported manufactured goods means structural FX pressure persists.

- External Debt Service: External debt rose 5.9% to ₦74.4trn in FY 2025. With the $6bn multilateral borrowing approved, future debt service obligations will intensify, creating a persistent and growing structural source of FX demand from the government over the medium term.

- FPI Repatriation Risk: The recently released Q1 2026 data showed FPI inflows surging to $9.86bn, creating significant latent repatriation risk. While net equity outflows eased to $6.61bn in April from $7.47bn in March, the scale of accumulated inflows means any deterioration in global risk sentiment could trigger a sharp spike in FX demand.

- Speculative Dollar Demand: The official-parallel market spread narrowed to 2.01% in May from 3.67% in April, equivalent to a tightening from ₦50/$ to ₦23/$. This real-time improvement in pricing alignment reduces arbitrage and speculative dollar hoarding incentives.

Other Channels

- Inflation (Energy Prices): Inflation has resumed an upward trend, driven by elevated energy prices feeding through PMS costs and imported inflation. This stokes broader FX demand from import-dependent sectors and erodes the real purchasing power of the Naira.

- CBN Monetary Policy Rate: The CBN held the MPR at 27.50% in May, pausing its tightening cycle amid global uncertainty and domestic inflation. Holding rates maintains real yields, helping to retain FPI flows and limit capital outflows in a volatile global environment.

- Foreign Reserves & CBN Intervention: Reserves rebounded 1.86% to $49.26bn in May 2026, reversing two months of decline. Stronger buffers enhance CBN’s intervention capacity and FX supply.

Net Assessment

Supportive - Crude Oil, Capital Importation, Trade Balance, Remittances, Import Dependency, Speculative Dollar Demand, and Foreign Reserves & CBN Intervention

Mixed - External Borrowing and CBN Monetary Policy Rate

Pressuring - External Debt Service, FPI Repatriation Risk, and Inflation (Energy Prices)

With 6 positive fundamentals outweighing 2 negative indicators (rising debt service and FPI repatriation risk) and 2 neutral indicators (CBN MPR hold and external borrowing), the Naira is positioned for greater stability in June. The persistence of the US-Iran conflict will sustain elevated oil prices, reinforcing Nigeria's positive FX fundamentals. However, escalating US-Europe tariff tensions risk reigniting a broader global trade war, dampening risk appetite and potentially reversing capital flows.

Why Does This Matter?

Inflation resuming an upward trend from energy prices is raising cost pressures and foreign exchange demand from import-dependent sectors. At the same time, potential foreign portfolio investment (FPI) repatriation following the outsized Q1 2026 surge could trigger significant foreign exchange demand and market volatility. Additionally, external debt rose to ₦74.4 trillion (+5.9%), amplifying debt service demands and pressure on external accounts. The legislative approval of $6 billion in external borrowing will further increase future debt service obligations and foreign exchange outflows.

Record crude production (1.66mbpd), combined with elevated Bonny Light prices ($126.71/b), should deliver strong oil revenue and export earnings in 2026. In addition, a persistent trade surplus (₦7.55trn in Q1 2026), surging capital inflows, and rebounding foreign reserves provide a structurally supportive foreign exchange backdrop.

What’s Next for June 2026?

In June, we expect the Naira to appreciate, supported by improved FX supply, stronger investor sentiment, and CBN strategic interventions. However, lingering geopolitical tensions, ongoing US-Iran conflict are likely to sustain subtle exchange rate volatility despite the temporary ceasefire between Israel and Lebanon.

We expect the Naira to trade within ₦1,360 - N1,370/$ (NFEM) and ₦1,375–₦1,393/$(BDC) in June 2026.

If you would like to explore the full analysis, you can download the full FX Market Report.