Nigeria’s Debt Sustainability Report 2025

Nigeria’s public debt has continued to grow at a faster pace than its revenue, with total public debt expanding at a 5-year CAGR of 37.2% against a revenue CAGR of 26.5%. The rapid debt growth stems from the widening budget deficits, exchange rate depreciation, and securitized Ways & Means.

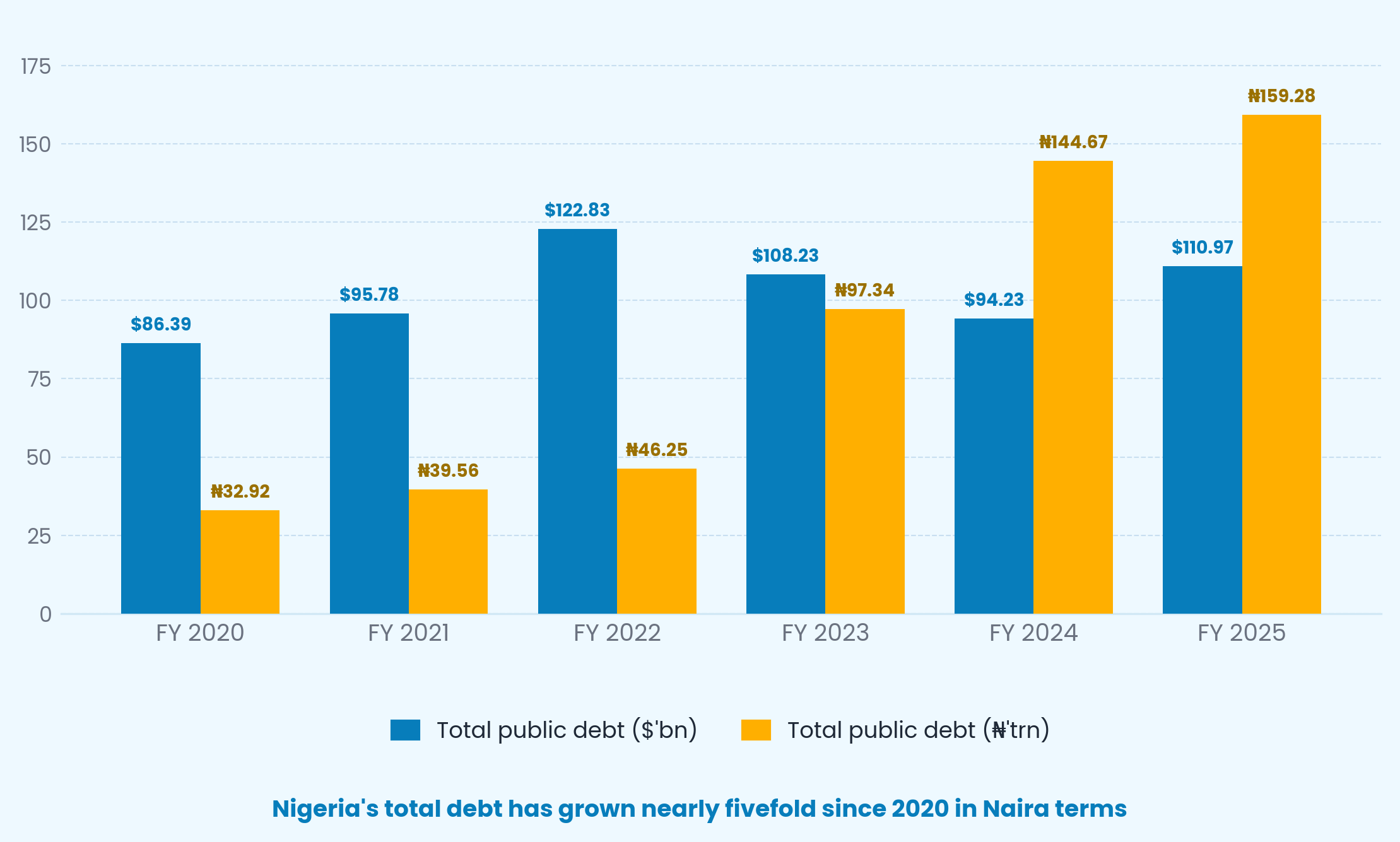

Total public debt increased by 10.1% year-on-year in Naira terms to N159.28trn in 2025, reflecting a combination of new borrowing activity and improved exchange rate compared to 2024 when Naira depreciation triggered a 49% jump in total debt in Naira terms and a 13% contraction in Dollar terms.

In 2025, Nigeria accessed a total ofN31.01trn in new loans, which is broken down into $2.53bn Eurobond issuance,N5.26trn raised through domestic bond issuances, N15.01trn from T-bill issuances, and cumulative borrowings of $4.95bn from multilaterals, including Afreximbank, AfDB, and the World Bank, reflecting continued reliance on both domestic and concessional external financing to support fiscal funding needs.

There is a mild correlation between Nigeria’s total public debt and foreign reserves, with reserves generally improving during periods of increased external financing, especially in 2024 and 2025.

A Growing Appetite for External Borrowing

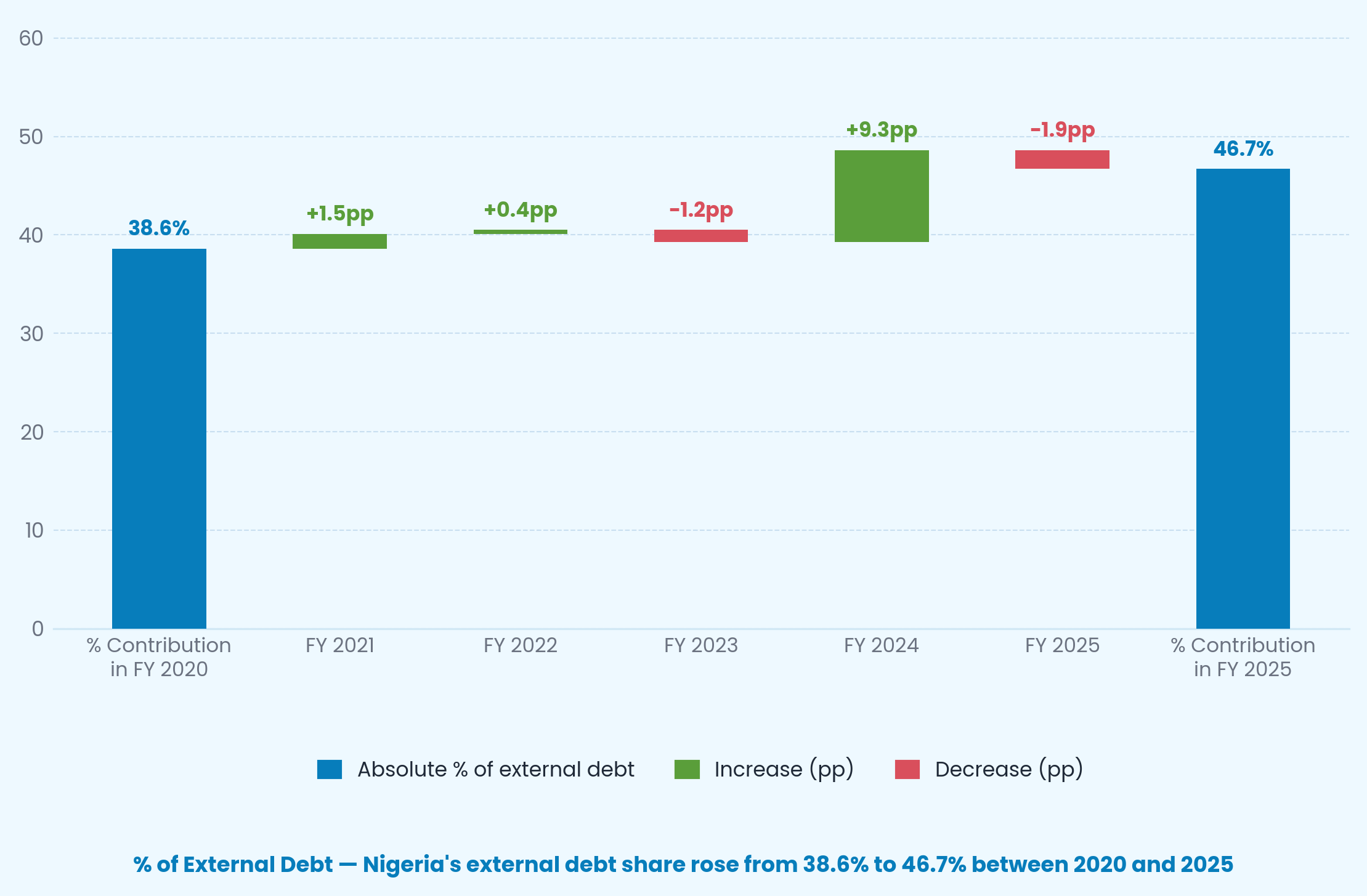

Between 2020 and 2023, Nigeria relied significantly on domestic borrowing, with external debt accounting for about 39–40% of total public debt. This shifted in 2024, following the DMO’s updated debt strategy, which targets a more externally balanced 45:55 (domestic-to-external debt mix).

In line with this, the external debt share increased by 10pp to 49%, supported by exchange-rate valuation effects, Nigeria’s re-entry into the Eurobond market after a two-year pause, raising $2.2bn in December 2024 and $2.53bn in November 2025 and loans from multilateral institutions. Although the share eased slightly to 47% in2025, the portfolio remains above historical levels and continues to move toward the revised strategy, supported by relatively cheaper external funding costs of 6%–9.5%.

The reappears to be a subtle but deliberate reduction in domestic financing activity. The Federal Government has consistently allotted at or below its stated offer sizes across both FGN bond and NTB auctions throughout 2025, despite sustaining some of the largest subscription volumes on record.

This moderation in domestic issuance, alongside the CBN’s enforcement of the 5% Ways and Means limit and a projected ₦31.46tn fiscal deficit in 2026, suggests an increasing need to diversify funding sources beyond the domestic market.

We believe this shift is already underway, evidenced by the legislative approval of $6bn in external borrowing from multilateral institutions, reinforcing a stronger policy tilt toward foreign financing in 2026.

Nigeria’s Debt Risk Is No Longer About Size but Repayment Capacity

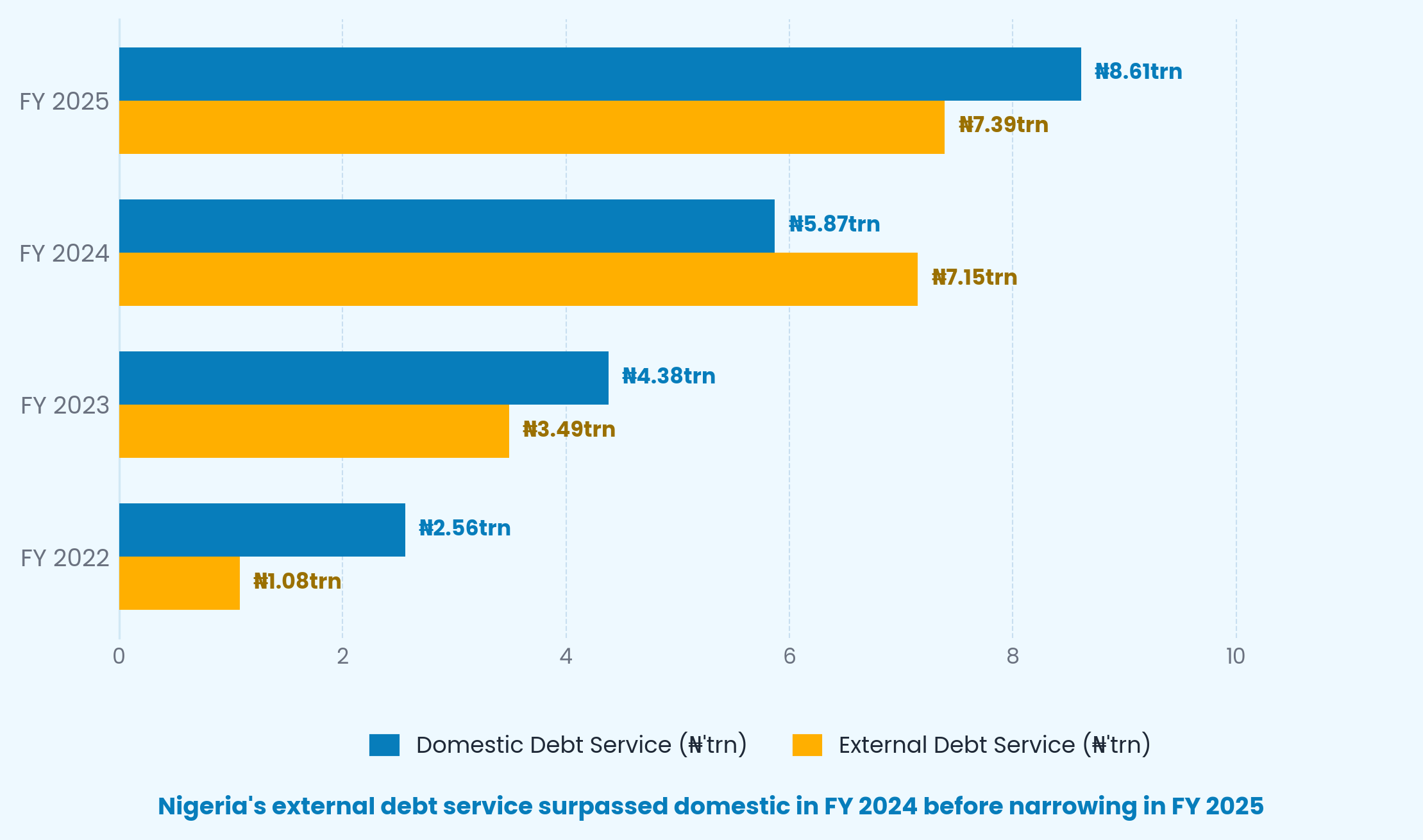

Beyond the elevated debt stock, Nigeria’s ability to service its rising debt obligations remains a concern, as revenue continues to grow more slowly at 14%Y-o-Y than debt-service commitments at 23% Y-o-Y. The debt service to revenue averaged about 63% in the last 2 years. Other key indicators such as debt-service-to-expenditure and debt-to-revenue remain above recommended threshold, keeping the country in the fiscal risk zone. Despite this, there is an increasing appetite for borrowing, especially from external sources, which may appear cheaper in the short term, however, potential exchange-rate depreciation could raise repayment costs over time, sustaining fiscal vulnerabilities.

Headline solvency indicators appear supportive, with the debt to GDP ratio moderating to 36.1%, partly reflecting the impact of the GDP rebasing exercise. However, this metric speaks more to borrowing capacity than debt sustainability. Servicing indicators provide a clearer picture of fiscal pressure, suggesting Nigeria could be approaching a scenario where nearly 70% of government revenue is consumed by debt servicing, leaving limited funds for CAPEX and recurring expenditure.

Nigeria’s debt service burden measured by its debt service/revenue ratio is expected to remain elevated in 2026, reflecting increased external borrowing and the risk of higher funding costs and exchange-rate pressures amid persistent geopolitical tensions.

Subnationals Continue to Rely on External Borrowing

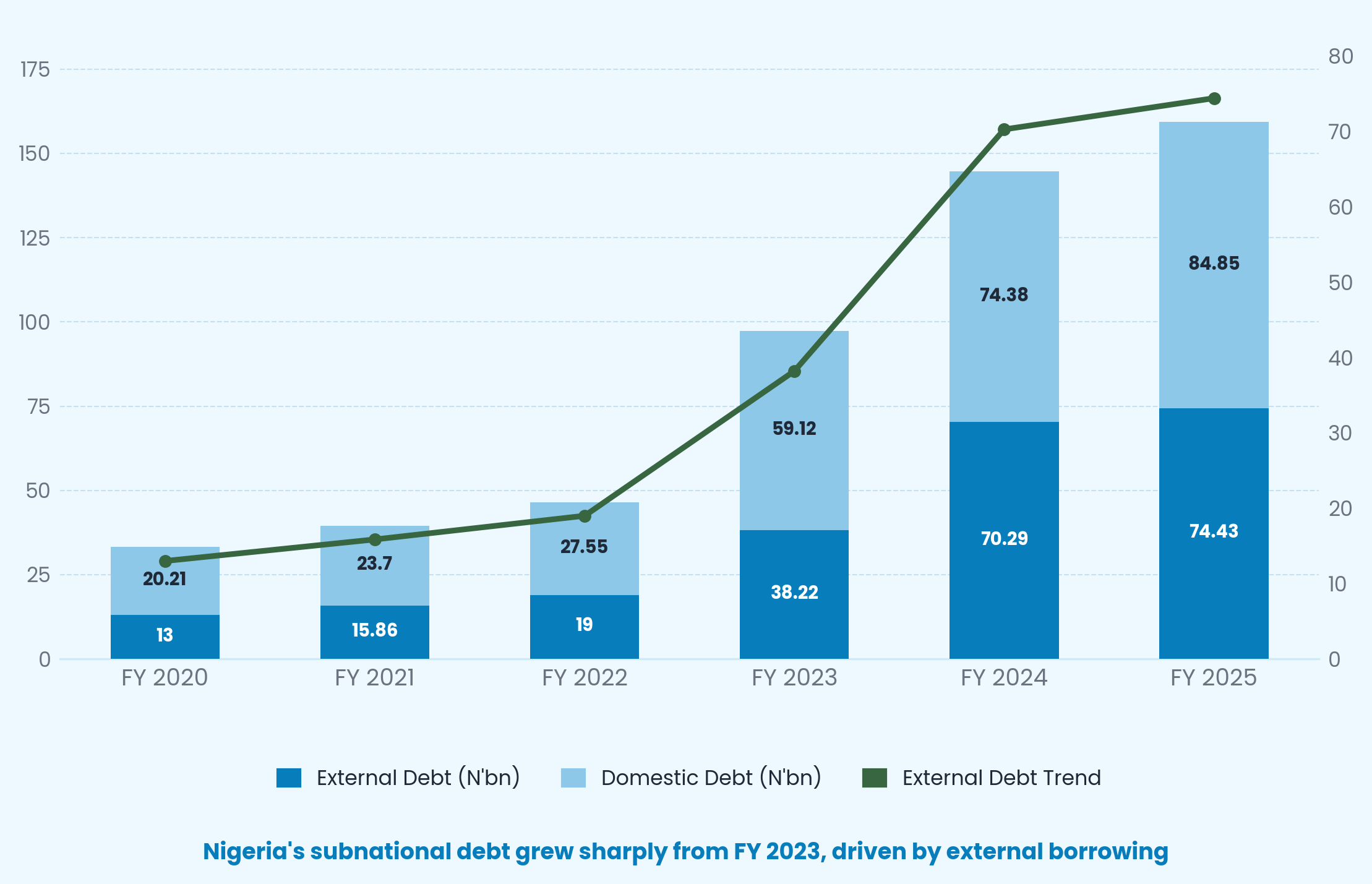

Despite the significant increase in FAAC allocations to subnationals, their debt stock continued to expand, reaching N12.52trn as of December 2025.

Nigerian states continue to rely more on external borrowing than domestic financing, with external debt rising by 18.4% YoY to N8.16trn in 2025, compared with a 17.5% increase in domestic debt to N4.36trn. External debt accounted for roughly 65% of total subnational debt in both 2024 and 2025, revealing sustained exposure to foreign-currency liabilities.

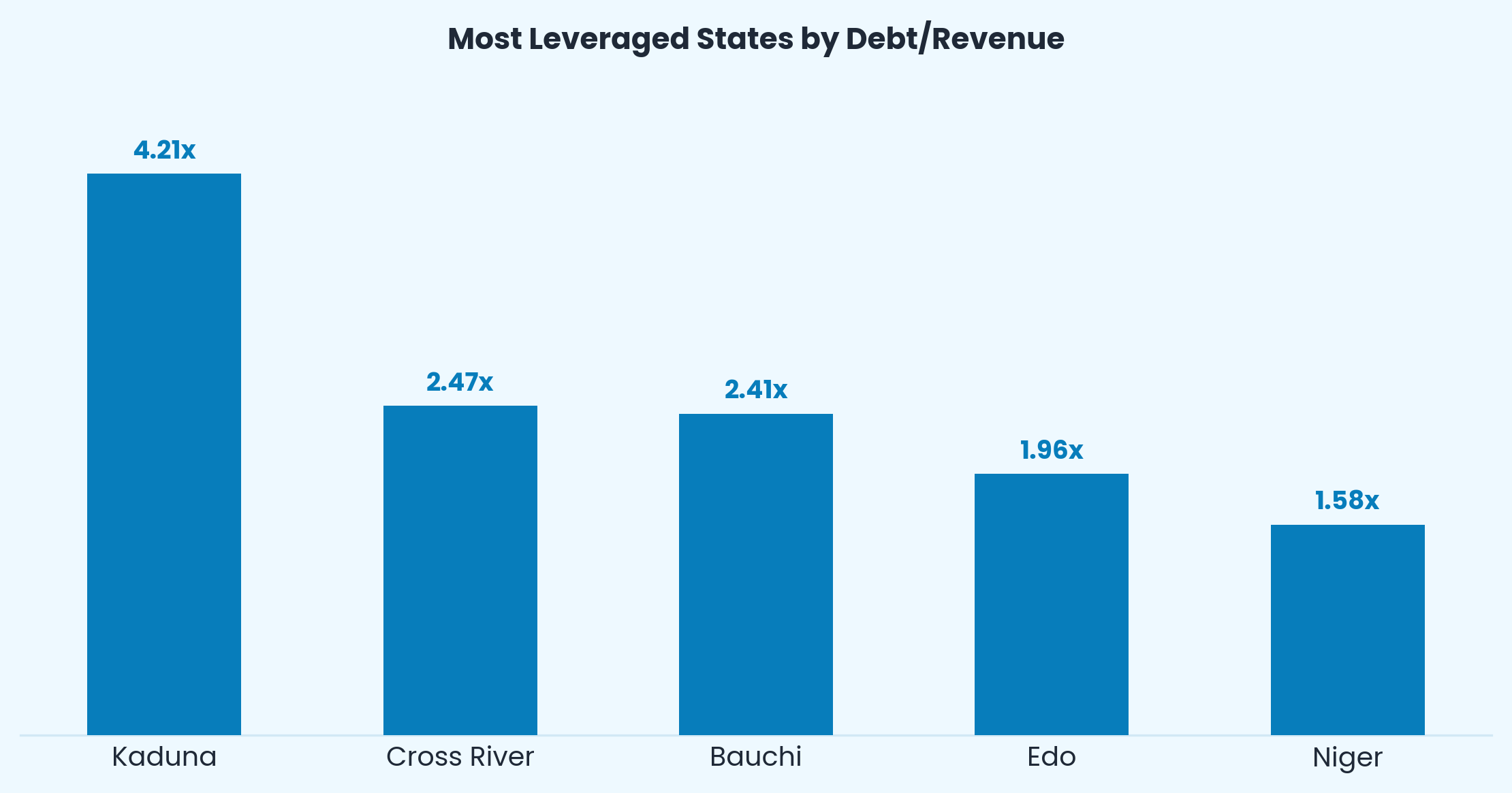

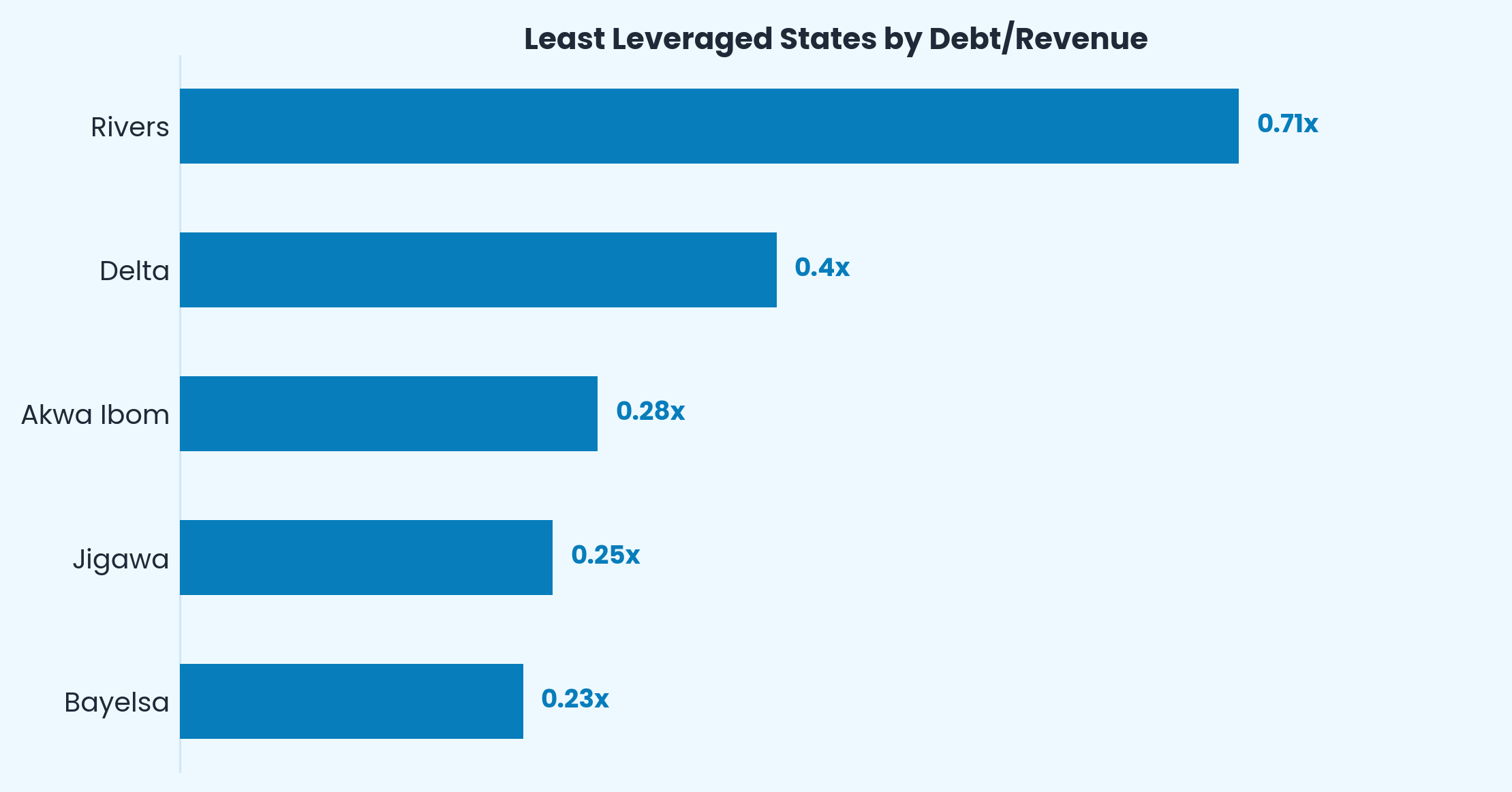

Using our forecasted 2025 IGR and actual FAAC, Bayelsa has the lowest repayment risk while Kaduna has the highest. Lagos, Kaduna, and Rivers account for 37% of the total subnational debt in 2025.

Oil-producing states have stronger debt repayment capacity due to higher federation inflows relative to other states. Kaduna faces the highest repayment pressure based on debt stock-to-total revenue, ahead of Cross River and Edo.

Subnational debt is expected to rise in 2026 as exchange-rate appreciation may moderate FAAC inflows, partly offset by stronger oil prices. In addition, increased spending on infrastructure and other development projects ahead of the 2027 governorship elections in several states could require additional borrowing, with total subnational debt projected to exceed ₦15tn.

How will Nigeria’s Debt Look like in 2026

Structural Position

Nigeria's debt risk is principally one of repayment capacity, not stock size. With debt servicing absorbing nearly two-thirds of government revenue and the interest-only-to-revenue ratio at 32.9% against a 12% IMF benchmark, the headline debt-to-GDP ratio of 36.1% understates the underlying fiscal pressure.

The pivot toward external financing reduces domestic crowding-out but introduces exchange rate pass-through risk that could rapidly erode the apparent cost advantage of foreign borrowing.

Near-Term Outlook

Elevated oil prices provide a revenue cushion, though this remains contingent on geopolitical conditions that are outside Nigeria's control.

The Nigeria Tax Act is the most structurally significant revenue reform in years, and the appointment of its principal architect as Finance Minister strengthens implementation credibility. However, with the VAT rate increase moderated in parliament and digital compliance infrastructure still developing, material revenue gains are more likely to crystallize in the medium term than within 2026.

With a ₦31.46trn projected deficit and debt service continuing to outpace revenue growth, 2026 is best characterised as a year of fiscal consolidation in progress rather than completion.

Going forward, The Eurobond maturity cycle between 2027 and 2034, totaling $11.4bn, is expected to increase debt service pressures, underscoring the urgency of sustained revenue reform and fiscal consolidation before these obligations fall due at scale.

Conclusion

Nigeria’s sovereign credit profile improved in 2025 following rating upgrades by Moody’s and Fitch, reflecting stronger external buffers, FX reforms, and improved macroeconomic policy credibility. This positive momentum should persist into 2026 and should support refinancing prospects ahead of the $11.4bn Eurobond maturity hump between 2027and 2034. However, the outlook is likely to remain stable with cautious upside potential, as elevated debt service burdens, might constrain the pace of further upgrades.

Download the full 2025 Debt Sustainability Report for a detailed breakdown, technical analysis, and 2026 Outlook.