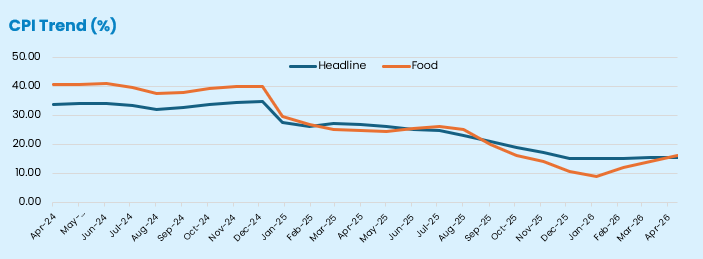

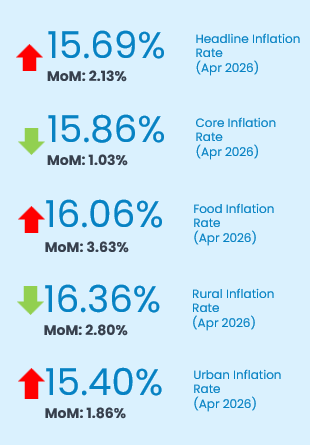

Headline inflation rose for the second consecutive month to 15.69% YoY in April from 15.38% in March, although the pace of monthly price increases moderated significantly to 2.13% MoM from4.18% in March.

Food inflation remained elevated at 16.06% YoY, driven by persistent increases in staple food items including millet, yam flour, beef, garri, beans, tomatoes, wheat grain, guinea corn, and plantain, according to NBS data.

Core inflation slowed materially on a monthly basis to 1.03% from 4.03% in March, but annual core inflation remained high at 15.86%, indicating continued broad-based inflationary pressures across the economy.

Inflationary pressures in April were largely driven by higher energy and transportation costs, with average PMS prices rising by 13.8% on average during the month, while imported food and farm produce inflation also remained elevated despite relative exchange rate stability.

State Focus

South-East recorded the highest food inflation at 21.56% and North-East (17.13%) recorded the highest all item inflation in April. Sokoto recorded the highest year-on-year all-items inflation rate at 25.7%, followed by Bauchi (22.5%) and Zamfara (22%), reflecting persistent supply-side and structural pressures. Conversely, Edo (5.9%), Borno (6.7%), and Jigawa (7.0%) recorded the slowest increases in headline inflation.

On a month-on-month basis, Niger (5.7%), Kano (4%), and Plateau (4.4%) recorded the highest increases, while Bayelsa (0.6%), Enugu, Rivers, and Ogun (1%) saw the slowest price growth. In food inflation, Enugu (32.7%), Kwara (30.8%), and Adamawa (30.1%) recorded the highest year-on-year increases, while MoM Kebbi (0.2%), Katsina (0.5%), and Bayelsa (1.3%) recorded the slowest rise.

April Inflation Signals

Headline inflation rose marginally to 15.69% YoY in April 2026 from 15.38% in March, marking the second consecutive monthly increase in annual inflation. However, month-on-month inflation slowed materially to 2.13% from 4.18% in March, suggesting that while inflationary pressures remained elevated during the month, the pace of price acceleration moderated compared to the sharp energy-induced shock recorded in March.

Food inflation remained a key driver of the uptick, with prices of staple commodities such as millet, yam flour, beef, garri, beans, tomatoes, wheat grain, guinea corn and plantain continuing to rise strongly across major markets.

Core inflation offered the most encouraging signal, easing to 15.86% YoY with MoM falling sharply to 1.03% from 4.03%, suggesting that the cost pass-through into services and non-food goods that characterised March may be unwinding. Although the annual core inflation rate remained elevated at 15.86%, indicating that inflationary pressures remain broad-based beyond food.

At the state level, Sokoto (25.74%), Bauchi (22.52%), and Zamfara (22.03%) anchored the top of the headline distribution, a North-West cluster whose persistent elevation maps directly onto insecurity-driven supply disruption and poor logistics infrastructure. On food inflation, 6 states (5 in the North-Central region) led MoM acceleration above 6% with Niger's 8.53% MoM the largest, signalling acute supply disruption in the North-Central food belt ahead of the lean season.

At the other end, Edo (5.91%), Borno (6.72%), and Jigawa (7.04%) posted the lowest YoY reads, though Borno’s relatively subdued inflation figure likely reflects weaker market activity and supply chain disruptions due to insecurity rather than genuine disinflation.

In May, we expect inflationary pressures to remain elevated within the 15.7–16% range and MoM toward 1.5–2.5% largely depending on developments in global energy markets and the sustainability of recent exchange rate stability. However, food supply conditions in the North-Central during the ongoing lean season remain the primary upside risk to the May inflation print.

We expect the MPC to retain the MPR at 26.5% at the upcoming meeting, as the second consecutive increase in annual inflation and elevated system liquidity conditions continue to support a cautious policy stance. While the sharp moderation in month-on-month inflation may reinforce the view that March’s spike was temporary, we believe the committee is still likely to maintain a cautious stance.

May 2026 Outlook

There may be higher global oil prices due to Iran conflict raise PMS, transport, and logistics costs, increasing upside pressure on May m-o-m inflation. Also, the lean season and persistent insecurity may keep disrupting food supply chains.

With stronger oil prices Nigeria's FX earnings and external liquidity position, may improve which could partially cushion imported inflation pressures if the Naira remains stable.

Additionally, lower expected landing costs for imported goods due to reduction in import duties on key commodities could mean a new tariff regime could ease inflation pressures in the near term.

Download the Full April 2026 Inflation Report

For detailed state-by-state breakdowns, technical analysis, and our May Outlook commentary, download the complete report.